We first select only the income statement accounts.

Ordering the Income Statement Accounts

The income statement shows revenues first, followed by expenses.

Revenues

The primary source of revenue is listed first in the revenue section of the income statement. Other streams of revenue are also listed separately if significant.

Expenses

The expenses side of the income statement starts with the cost of goods sold and any other direct expenses incurred to produce revenue. This gives you the gross margin from the business.

Operating Expenses

Other operating expenses, such as research and development expenses, sales and general administrative expenses, etc., are then listed in the income statement. These are deducted from the gross profits to give you the operating profits from the business.

Non-operating Income & Expenses

We then list the non-operating expenses and non-operating income, such as interest income, interest expenses, and gains or losses on the sale of assets. The sum of these, deducted from operating profits, gets you the total income before taxes.

Taxes & Net Income

We then deduct income taxes from total income before taxes to arrive at the net income. You have prepared a completed income statement when you have ordered the revenue and expenses, computed and deducted taxes to arrive at the net income. Remember that the income statement accounts are temporary accounts. All these accounts are reset to zero at the end of the period. However, if you have followed the process correctly, the final result of the income statement, the net income of the period, would have been carried over to the balance sheet and will be reflected in the retained earnings account.

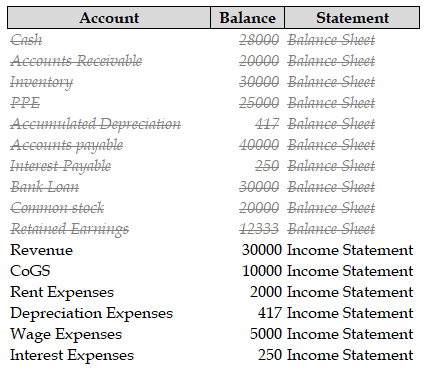

Income Statement Ordered

The income statement ordered with revenues on top followed by expenses is presented below. The net income from the income statement is transferred to the retained earnings account in the balance sheet.

The income statement accounts are ‘temporary accounts’ and the balance are transferred to the retained earnings. So at the end of an accounting period the balances are rest to zero and start at zero at the beginning of each accounting period.