Transactions can be classified into two types of transactions by when they occur: 1) in-period transactions and 2) end-of-period transactions.

In-period transactions are transactions that happen daily in the course of the company’s business activities. You have finished recording them on a daily basis throughout the accounting period.

The end-of-period transactions are transactions that are recorded at the end of the period, usually to account for changes in revenues, expenses, assets, or liabilities due to the passage of time or usage of an asset. In the traditional accounting system, this step is called adjusting entries.

An example of revenue creation due to the passage of time is the recognition of a sale of a magazine subscription. An example of the creation of a liability due to the passage of time is the recognition of a rent payable at the end of a month/year. An example of an expense with the usage of an asset is depreciation or amortization of an asset.

Adjusting entries are journal entries made at the end of an accounting period to ensure that a company’s financial statements accurately reflect its financial position and performance. These entries are necessary because of the accrual method of accounting. The accrual method records transactions when they occur, not necessarily when the cash is exchanged.

Adjusting entries ensure that the income statement (which shows revenues and expenses) and the balance sheet (which shows assets, liabilities, and equity) are up-to-date and accurate at the end of the accounting period. This process is crucial for producing financial statements that provide a true and fair view of a company’s financial position and performance. Adjusting entries are typically made at the end of the year, but before financial statements are prepared. Common examples of adjusting entries include recording depreciation on fixed assets, recognizing bad debts, and adjusting inventory values. These entries help accountants adhere to the matching principle, which states that expenses should be recognized in the same period as the revenue they help generate, leading to a more accurate representation of a company’s financial health.

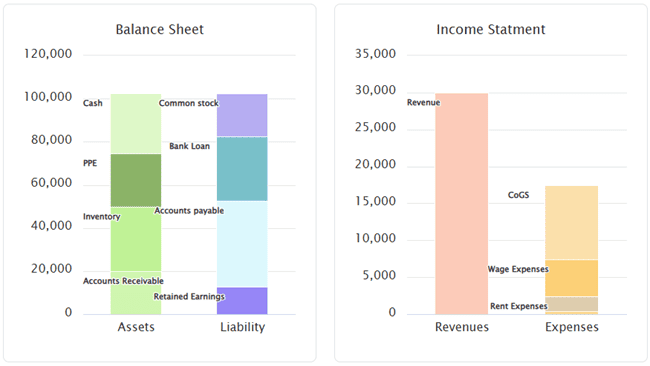

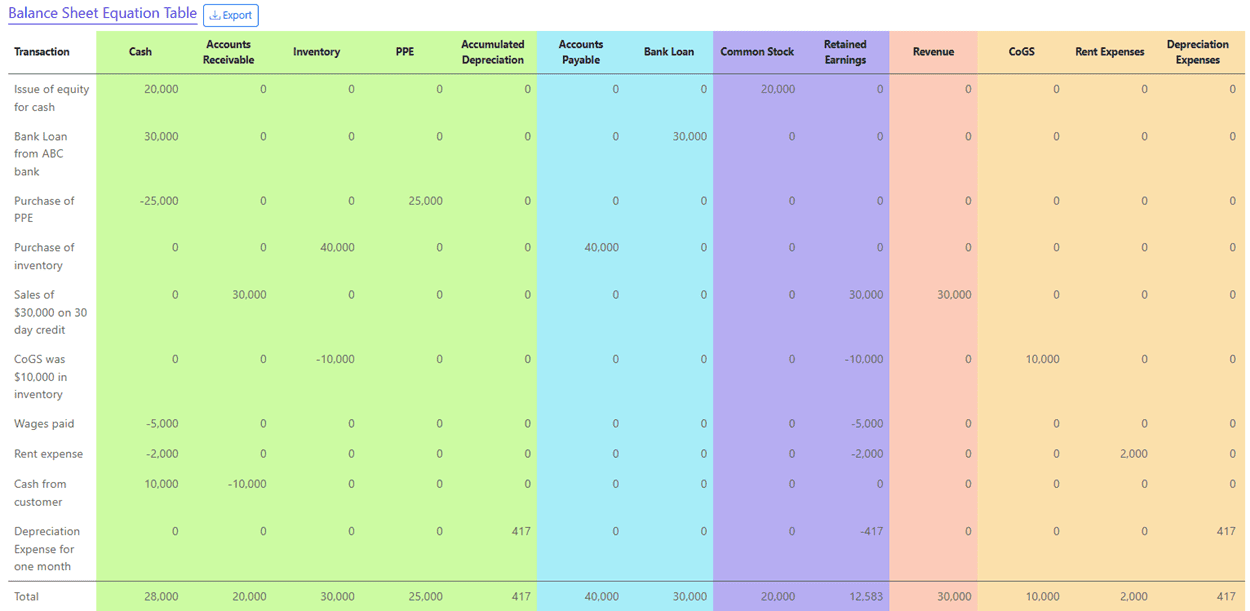

The 10th transaction in our illustration is an end-of-the-period entry. We are accounting for the value of the machine used due to the passage of time.

Transaction 10: The company’s equipment would live for 5 years and used the straight-line depreciation method to account for depreciation expenses.

- The use of equipment reduces its value. This has a financial impact on the company as it reduces its asset value. The reduction in value is captured in an account called the accumulated depreciation account. The accumulated depreciation account offsets the PPE account which carries the gross value of the asset. Accounts that offset other accounts are called as contra asset accounts.

Since the equipment is used to generate revenues, the associated value used is considered as an expense and must be recorded as a depreciation expense. This transaction must be reflected in the accounting system. - The accounts impacted are:

- Accumulated depreciation account.

- Depreciation expenses.

- The type of accounts impacted are:

- Accumulated depreciation account is classified as asset (contra) account.

- Depreciation expense account is classified as an income statement – expenses account.

- The direction of the impact is listed below.

- Accumulated depreciation account balance increases.

- Depreciation expenses balance increases.

- The quantity of impact in each account should reflect the time that is being accounted for. Here we are talking about one month in a life of 5 years for the equipment. So the cost of the equipment $25,000 is divided by 5 for five years. This is then divided by 12 to account for 1 of twelve months. (25,000*(1/5)*(1/12)=416.7)

- Depreciation expenses increases by $417.

- Accumulated depreciation account increases by $417.

- Check if the BSE equation

- Sum of Assets : PPE via Accumulated depreciation $-417.

- Sum of Liabilities & Shareholders Equity : Retained Earnings (Revenues – Expenses) $-417.

The balance sheet equation template will be as follows.

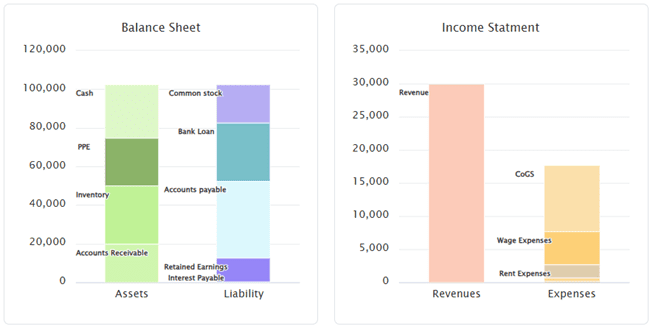

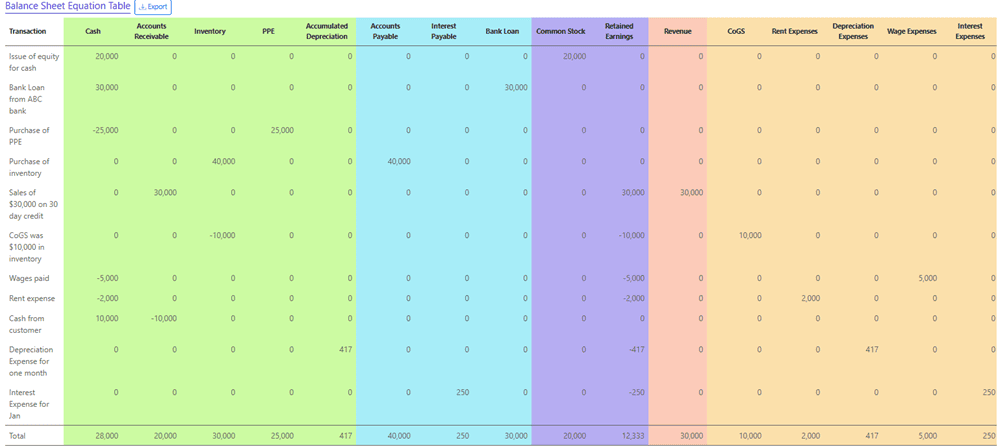

Transaction 11: Interest on Bank Loan

The company has a bank loan on which it pays a 10% interest. Since we follow the accrual system of accounting, we need to accrue the interest expense for the month of January even if we do not pay the interest.

- The passage of time has created an interest obligation and so there is a financial impact on the company. Interest is payable by the company. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Interest payable

- Interest expense

- The type of accounts impacted are:

- Interest payable is classified as a liability account.

- Interest expense account is classified as an income statement – expenses account.

- The direction of the impact is listed below.

- Interest payable balance increases.

- Interest expenses balance increases.

- The quantity of impact in each account is as follows:

- Interest payable increases by $250.

- Interest expenses account increases by $250.

- Check if the BSE equation balances.

- Assets Total: zero.

- Liabilities & Shareholders Equity Total: Liabilities $+250 & retained Earnings (Revenues – Expenses) $-250 so net zero.

Both the end-of-period transactions listed on this page happen to be small amounts and so are not visible on the balance sheet and income statment displayed above. These are, however, visible in the BSE template below.

Let us move to the next step which is summarizing these accounts.