The Accounting Equation or Balance Sheet Equation (BSE)

All assets must be paid for. Assets must be funded by someone. This funding comes primarily from two sources. Funding can come from the owners or from other sources. Funding from owners is referred to as shareholders’ equity. And funding from other sources is classified as liabilities.

Therefore, we can say that assets of a business are funded by liabilities and owner’s equity. The accounting equation simply represents this fact as an equation.

Assets = Liabilities + Shareholders Equity

The accounting equation is also known as the balance sheet equation (BSE) because the balance sheet is built on this equation.

BSE image

A balance sheet will balance only if the accounting equation is true.

The accounting equation is the foundation of the double-entry accounting system.

But where are the income statement accounts? Where are the revenue accounts and expenses accounts?

The Income Statement Equation or the Net Income Equation

You probably noted that the income statement accounts are missing in the accounting equation. Where are the revenue accounts and expenses accounts?

The income statement accounts are netted (Revenues – Expenses) into the retained earnings account in the balance sheet. This happens continuously at the point of every transaction. On every transaction that has income statement accounts, either revenues or expenses, we apply the income statement equation, revenues – expenses, and put the results in the retained earnings account into the balance sheet equation.

Revenues increase retained earnings because the income statement accounts are netted with the equation (Revenues – Expenses), all revenues will be positive and increase the retained earnings.

Whereas, when recording an expense, we will usually have no revenues. Therefore, applying the income statement equation (Revenues – Expenses) will result in a negative value and decrease the retained earnings.

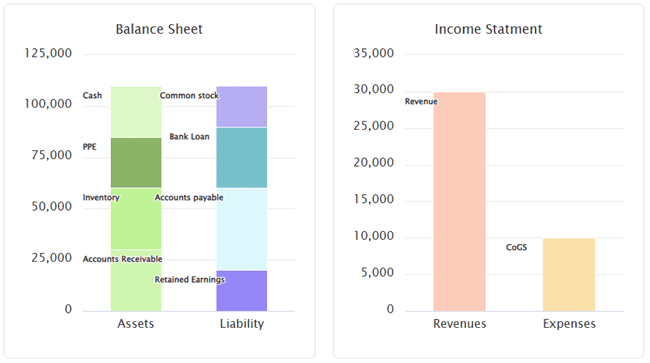

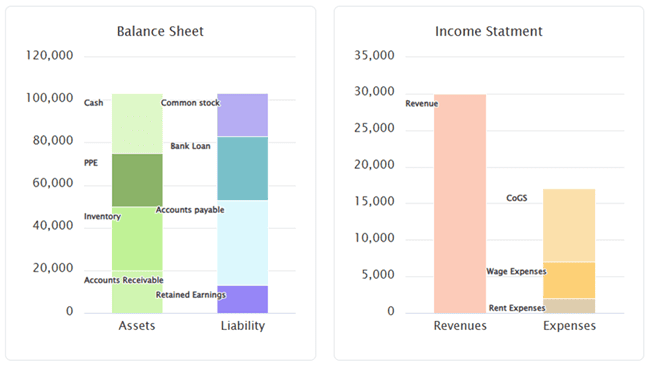

Balance Sheet Equation (BSE) Table

The balance sheet equation can be put into a table. All the asset accounts will be placed together. Similarly, all the liabilities and shareholders’ equity accounts will be placed together. The liabilities and shareholders’ equity accounts will be summed up to check if the balance sheet equation holds true at all points in time.

More details?

(Image)

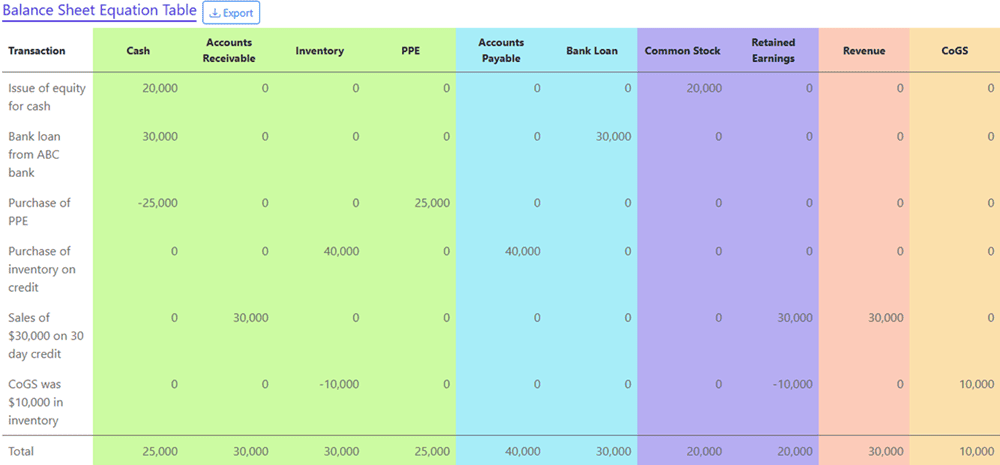

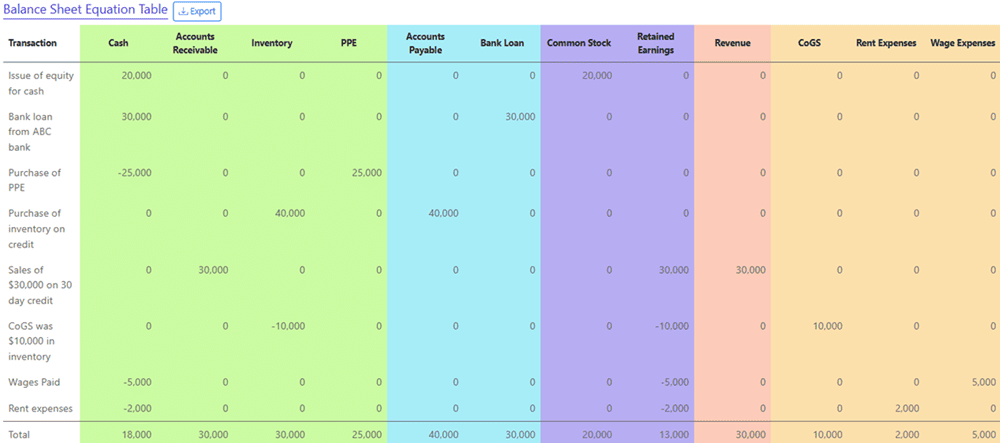

Recording the Transaction Analysis in the BSE Table

Once a transaction has been analysed, we transfer this information to the balance sheet equation. All impacted assets are either increased or decreased by the amounts they have been affected by.

Each row has the details of only one transaction. And each row must reflect the accounting equation with the sum of assets equal to the sum of liabilities and shareholders’ equity. We typically build this check in Excel on the far right of the balance sheet equation.

In our illustration above, we see that the cash account has decreased by $1000. So, we will subtract $1,000 in the cash account column (negative $1,000). We know inventory has gone up by $1000 and so we put in a positive $1,000 in the inventory column. Both cash and inventory are assets and therefore appear in the asset side of the balance sheet equation.

Illustration

We will analyze and record each transaction one by one.

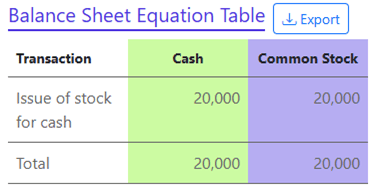

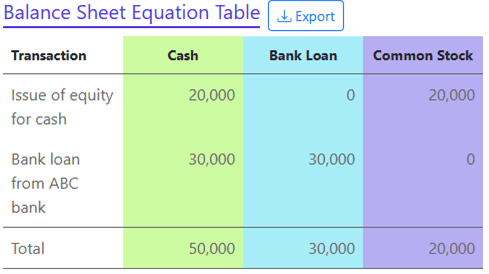

Mark invested $20,000 to start a business in exchange for 1,000 shares on January 1st.

- This activity has a financial impact on the company. Cash is received by the company. The company issues equity or common stock. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Cash

- Common Stock

- The type of accounts impacted are:

- Cash is classified as an Asset account.

- Common stock is classified as a Shareholders’ Equity account.

- The direction of the impact is listed below.

- Cash balances increase.

- Common Stock issued by the company increases.

- The quantity of impact in each account is as follows:

- Cash increases by $20,000.

- Common Stock increases by $20,000.

- Check if the BSE equation balances.

- Sum of Assets : Cash $20,000.

- Sum of Liabilities & Shareholders’ Equity : $20,000.

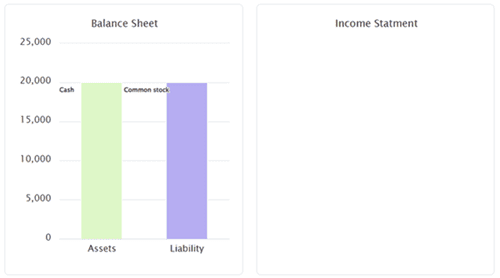

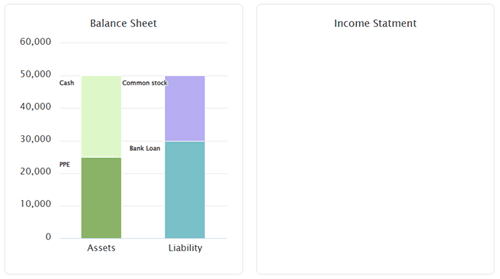

Balance Sheet after Issue of Equity

After Mark invested $20,000 to start a business in exchange for 1,000 shares on January 1st, the balance sheet and income statement will look as follows. Only two accounts – cash and common stock have balances. The balance sheet balances.

There has been no revenues or expenses and so the income statement is blank.

The balance sheet equation in Excel will look as above.

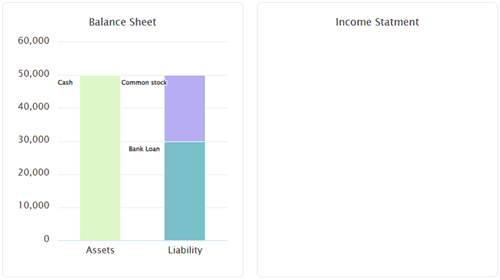

Transaction 2: The business borrowed $30,000 from ABC bank at an interest rate of 10% per year on January 1st.

- This activity has a financial impact on the company. Cash is received by the company. The company now has a liability to the bank. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Cash

- Bank Loan

- The type of accounts impacted are:

- Cash is classified as an Asset account.

- Bank Loan is classified as a Liability account.

- The direction of the impact is listed below.

- Cash balances increase.

- Bank Loan balance increases.

- The quantity of impact in each account is as follows:

- Cash increases by $30,000.

- Bank Loan balance increases by $20,000.

- Check if the BSE equation balances.

- Assets : Cash $30,000

- Liabilities & Shareholders Equity: Bank Loan $30,000

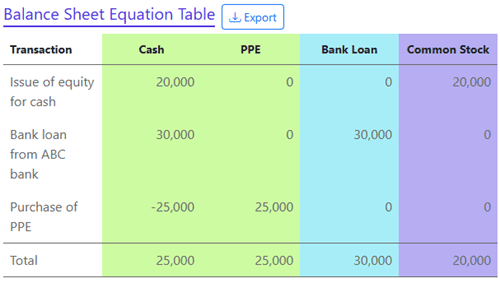

The BSE template will have a new column now – the Bank Loan column.

Transaction 3: Equipment worth $25,000 was purchased by the company in exchange for cash on January 4th

- This activity has a financial impact on the company. Cash is paid by the company. The company has received equipment which is an asset the company owns. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Cash

- Property, Plant and Equipment (PPE)

- The type of accounts impacted are:

- Cash is classified as an Asset account.

- PPE is classified as an Asset account.

- The direction of the impact is listed below.

- Cash balance decrease.

- PPE balance increases.

- The quantity of impact in each account is as follows:

- Cash decreases by $25,000.

- PPE increases by $25,000.

- Check if the BSE equation balances.

- Assets Total: Cash+PPE $-25,000 + $+25,000 = $0

- Liabilities & Shareholders Equity Total: No accounts impacted = $0

Note here that both the accounts impacted are asset accounts.

The BSE template will have a new column for PPE now.

Transaction 4: Inventory worth $10,000 of inventory was purchased by the company on 60 days credit on January 6th.

- This activity has a financial impact on the company. Inventory is received by the company. The company now has a liability to the vendor. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Inventory

- Accounts Payable

- The type of accounts impacted are:

- Inventory is classified as an Asset account.

- Accounts Payable is classified as a Liability account.

- The direction of the impact is listed below.

- Inventory balances increase.

- Accounts Payable balance increases.

- The quantity of impact in each account is as follows:

- Inventory increases by $10,000.

- Accounts Payable balance increases by $10,000.

- Check if the BSE equation balances.

- Assets Total: Inventory $10,000

- Liabilities & Shareholders Equity Total: Accounts Payable $10,000

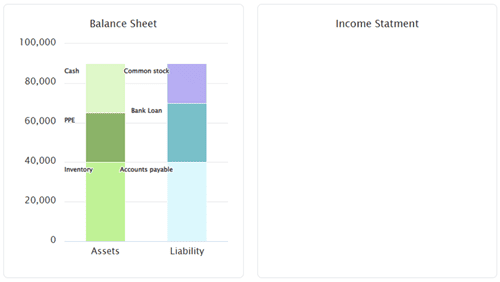

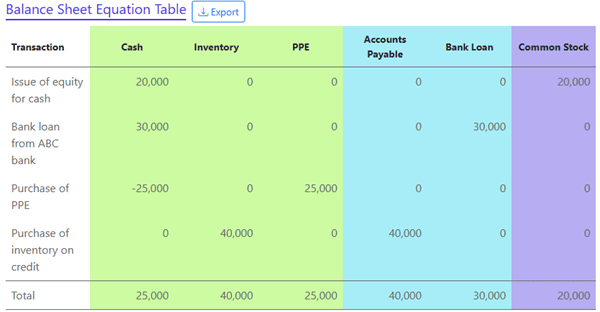

The BSE template will look as follows.

Transaction 5: Three customers walked into the store to enquire about prices and products on January 12th.

- No Financial Impact. No transaction needs to be recorded.

Transaction 6: The company sold $20,000 worth of inventory for $30,000 on 30 day credit on January 15th.

- This activity has a financial impact on the company. The company earns revenues. The customer owes the company the value of goods. The company’s inventory balances have declined. This transaction must be reflected in the accounting system.

- When goods or services are sold and revenue is recognized, we need to account for two distinct ways the company is impacted. The accounts impacted are:

- Revenue recognition:

- Revenues need to be recorded. Receipt of payment or creation of an accounts receivable .

- Recognition of cost of goods sold:

- Cost of Goods Sold (COGS) expenses acknowledged.

- Reduction of inventory balances.

- Revenue recognition:

- The type of accounts impacted above are:

- Revenue is classified an Income Statement – Revenues Account.

- Accounts receivable is classified as an Asset account.

- Cost of Goods Sold (COGS) expenses is classified an Income Statement – Expenses Account.

- Inventory is classified as an Asset account.

- The direction of the impact is listed below.

- Revenues balance increase.

- Accounts receivable balance increases.

- CoGS goods balance increases.

- Inventory balance decreases.

- The quantity of impact in each account is as follows:

- Revenues balance increases by $40,000.

- Accounts receivable balance increases by $40,000.

- CoGS goods balance increases by $10,000.

- Inventory balance decreases by $10,000.

- Check if the BSE equation balances.

- Sum of Assets : Accounts receivable + Inventory $+40,000 + $-10,000 = $30,000

- Sum of Liabilities & Shareholders’ Equity : Retained Earnings (+Revenues-CoGS)= $+40,000+$-10,000= $30,000

Note: We see the income statement accounts active for the first time. In this transaction, you will see both revenues and CoGS expenses are added to the income statement. Note also that the revenue has increased the retained earnings and the CoGS has reduced the retained earnings. The difference between the revenues and expenses is what is added as the retained earnings in the balance sheet below.

Transaction 7: The company paid wages of $5,000 on January 31st.

- This activity has a financial impact on the company. Cash is paid by the company. The company has received services for which wages are being paid. Wages are an expense incurred by the company. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Cash

- Wage expenses

- The type of accounts impacted are:

- Cash is classified as an asset account.

- Wage expense account is classified as an income statement – expenses account.

- The direction of the impact is listed below.

- Cash balance decrease.

- Wage expenses balance increases.

- The quantity of impact in each account is as follows:

- Cash decreases by $5,000.

- Wage expenses account increases by $5,000.

- Check if the BSE equation balances.

- Assets Total: Cash $-5,000.

- Liabilities & Shareholders Equity Total: Retained Earnings (Revenues – Expenses) $-5,000.

Since wage expenses has been added to the income statement, the net income and consequently the retained earnings goes down bythe wage expenses of $5,000.

Transaction 8: The company’s rent for the month was $2,000 was paid on January 31st.

- This activity has a financial impact on the company. Cash is paid by the company. The company has received services for which rent is being paid. Rent is an expense incurred by the company. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Cash

- Rent expenses

- The type of accounts impacted are:

- Cash is classified as an asset account.

- Rent expense account is classified as an income statement – expenses account.

- The direction of the impact is listed below.

- Cash balance decrease.

- Rent expenses balance increases.

- The quantity of impact in each account is as follows:

- Cash decreases by $2,000.

- Rent expenses account increases by $2,000.

- Check if the BSE equation balances.

- Sum of Assets : Cash $-2,000.

- Sum of Liabilities & Shareholders Equity : Retained Earnings (Revenues – Expenses) $-2,000.

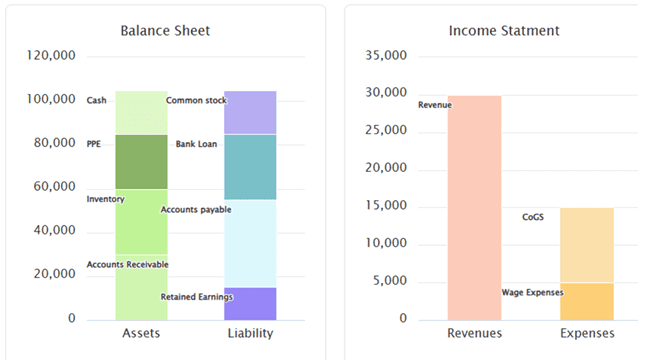

Since rent expenses has been added to the income statement, the net income and consequently the retained earnings goes down bythe rent expenses of $2,000. The BSE table below will have a new column for rent expenses.

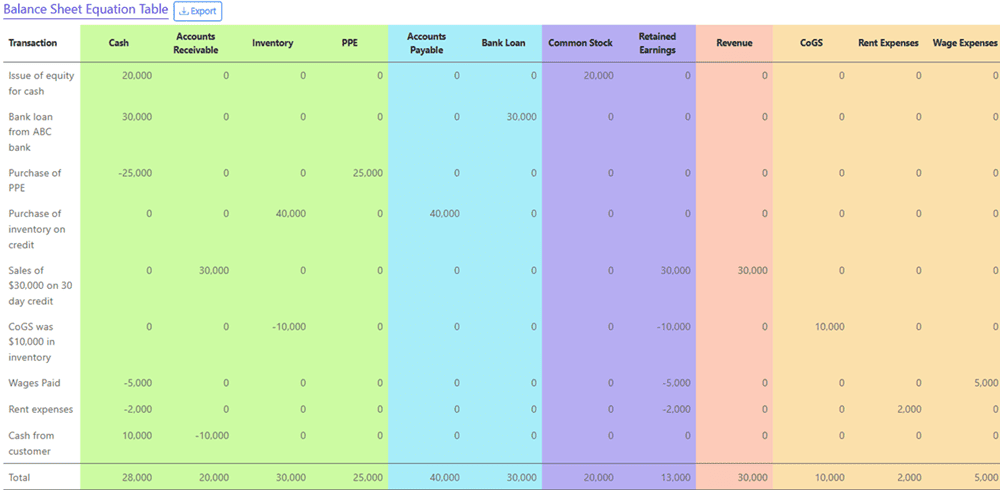

Transaction 9: On January 31st, $10,000 of accounts receivable was collected from the customer related to sales made on Jan 15th.

- This activity has a financial impact on the company. Cash is received by the company. The company has received cash from a customer who owed money to the company. Since he owes less money to the company, accounts receivable balance is also impacted. This transaction must be reflected in the accounting system.

- The accounts impacted are:

- Cash

- Accounts receivable

- The type of accounts impacted are:

- Cash is classified as an Asset account.

- Accounts receivable is classified as an Asset account.

- The direction of the impact is listed below.

- Cash balance increases.

- Accounts receivable balance decreases.

- The quantity of impact in each account is as follows:

- Cash increases by $10,000.

- Accounts receivable increases by $10,000.

- Check if the BSE equation balances.

- Sum of Assets : Cash+ Accounts receivable $10,000 + $-10,000 = $0

- Sum of Liabilities & Shareholders Equity : No accounts impacted = $0

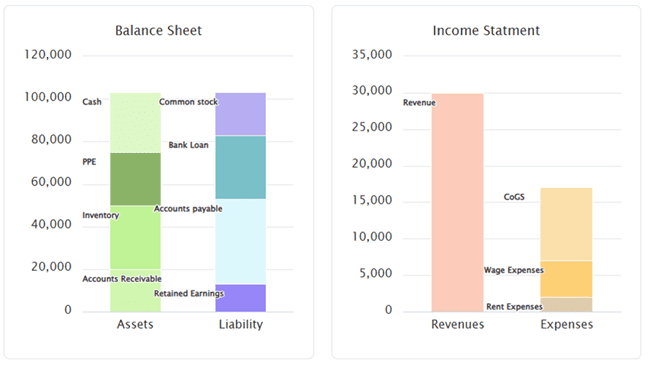

Note that there seems to be no change from the previous balance sheet as the total assets of $100,000 has not changed. However, if you look carefully, you will see that the cash balance has gone up and the accounts receivable balance has come down by the cash collected $10,000.

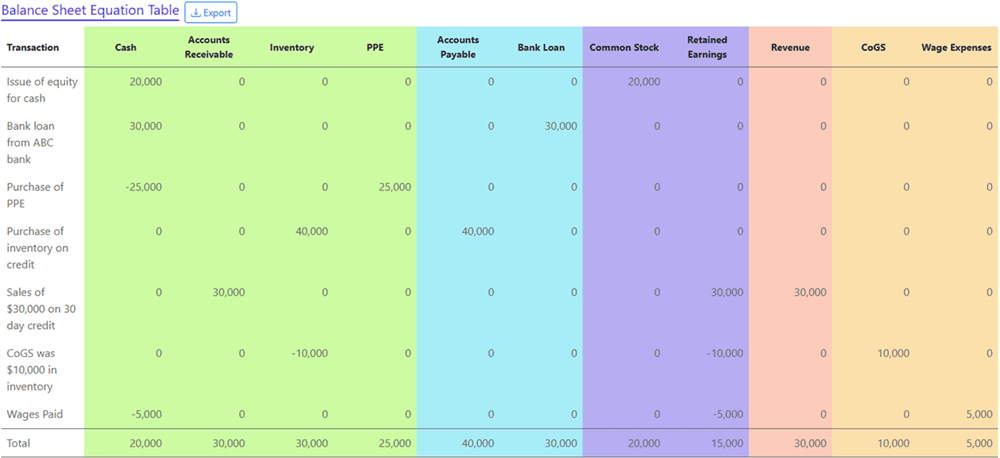

The BSE equation will look as follows.

Transaction 10 is an end-of-period entry. So we will deal with it in the next chapter.