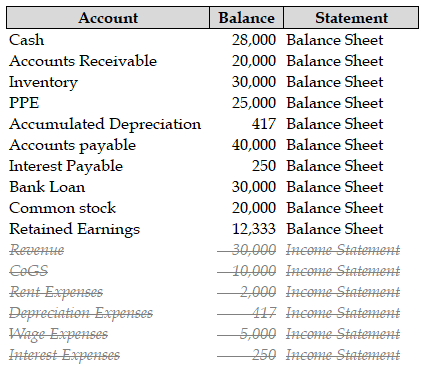

We first select all the balance sheet items.

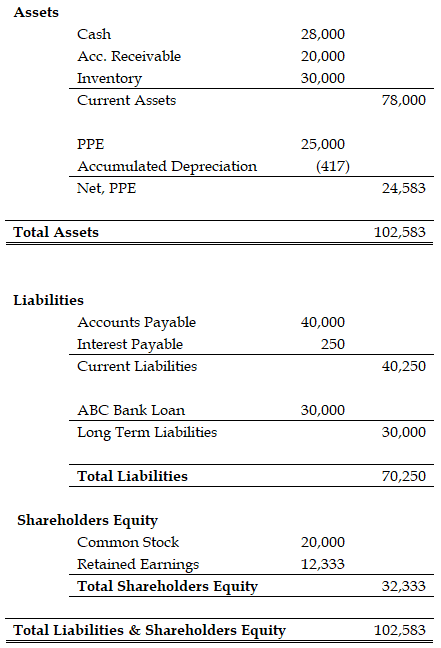

Three Lists that Form the Balance Sheet: Assets, Liabilities and Shareholders’ Equity

The accounts and their balances are categorized into three categories: assets, liabilities, and shareholders’ equity.

The sum of the asset accounts forms the total assets of the balance sheet. The sum of the asset accounts must equal the sum of the liabilities and shareholders’ equity accounts in the balance sheet.

Ordering the Assets in the Balance Sheet

The asset accounts are listed in order of their liquidity by convention. Current assets are usually assets that can be converted into cash within 12 months. Assets that have a longer life are categorised as long-term assets. Current assets are listed first. Within the current accounts, we order the assets according to liquidity, with the most liquid assets listed first, followed by less liquid accounts. Cash and cash equivalents account is right on top of the current assets accounts because cash and cash equivalents are the most liquid assets. Cash and cash equivalents are followed by accounts receivable, inventory, and other short-term assets, which are the current assets in a balance sheet. Current assets are totaled first before long-term assets are listed on the assets side of the balance sheet.

Long-term assets are listed after the current assets are sub-totalled. Long-term assets are also listed in order of their liquidity. Some companies have a subtotal for long term assets. Others do not. However, all companies sum the current assets and long-term assets, to get the total assets which ends the assets side of the balance sheet.

Ordering the Liabilities in the Balance Sheet

The liability accounts are also ordered by their liquidity by convention. Current liabilities are usually liabilities that need to be paid in 12 months or less. Liabilities that have a longer life, such as bank loans and lease liabilities, are categorised as long-term liabilities.

Current liabilities are listed first. And followed by long-term liabilities. The current liabilities accounts are also ordered in order of their liquidity, with the most liquid liabilities listed first. The accounts payable account is right on top of the current liabilities accounts list because it is considered the most liquid current liability given it is usually paid in a matter of days. Accounts payable is followed by notes payable, taxes payable, and other short-term liabilities. These current liabilities are summed up to get the total current liabilities section in a balance sheet.

Long-term liabilities are listed after the current liabilities section. These are also listed in order of their liquidity. Current liabilities and long-term liabilities are summed up to get the total liabilities section in a balance sheet.

Ordering the Shareholders’ Equity in the Balance Sheet

The shareholders’ equity section of the balance sheet is less governed by liquidity. By convention, the shareholders’ equity section of the balance sheet starts with common stock. Common stock is followed by its sister account, the additional paid-in-capital account. The additional paid-in-capital account is followed by treasury stock and retained earnings.

You have prepared a completed balance sheet when you have ordered the three components of the balance sheet and put them together. Notice that the sum of total assets is equal to the sum of total liabilities and total shareholders’ equity.

Ordered Balance Sheet

The ordered balance sheet of our illustrative company is presented below.

Note that the retained earnings matches the net income from the income statement because the net income is transferred to the retained earnings. The net income matches the retained earnings only because this is the first year of operations. In subsequent years the net income is added to the retained earnings balance and so the retained earnings will not match the net income of each year.